![]()

[Mar-2026] GAFRB Pre-Exam Practice Tests | Exam Questions and Answers for Government Financial Manager Study Guide

Examination 2: Governmental Accounting, Financial Reporting and Budgeting (GAFRB) Certification Sample Questions

AGA GAFRB Exam Syllabus Topics:

| Topic | Details |

|---|---|

| Topic 1 |

|

| Topic 2 |

|

| Topic 3 |

|

NEW QUESTION # 58

A city issues S100,000 of 10-year general obligation bonds on April 1, 2024. Debt service of $10,000 must be paid each year on March 31, with 5% interest paid on the unpaid balance. Based upon this information, the interest expense reported on the government-wide statement for fiscal year ending March 31, 2025, is

- A. $5,000.

- B. $ 3,750.

- C. $15.000.

- D. $ 4,500.

Answer: A

Explanation:

The city issues $100,000 in general obligation bonds on April 1, 2024, and the first principal payment of

$10,000 is due on March 31, 2025. The interest rate is 5% annually on the unpaid principal balance.

As of April 1, 2024, the full $100,000 is outstanding. For the full fiscal year (April 1, 2024 to March 31,

2025), interest accrues on the full amount until payment is made. The interest on $100,000 for one year at 5%

=

Interest Expense = $100,000 × 5% = $5,000

Note: Interest is typically calculated on the beginning-of-period balance, and since the payment is made at the end of the year (March 31, 2025), the full $5,000 interest is recognized for that year.

Relevant Standards and References:

GASB Statement No. 34, Basic Financial Statements for State and Local Governments GASB Codification Section 2200 (Government-Wide Financial Statements) GFOA Guidance on Long-Term Debt Accounting

NEW QUESTION # 59

Which type of cost is generally allowed for a grant under the OMB Uniform Guidance?

- A. materials and supplies

- B. lobbying expenses

- C. general government expenses

- D. interest payments

Answer: A

Explanation:

Under OMB's Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance), allowable costs under federal grants must be:

Necessary and reasonable for program performance

Allocable to the grant

In accordance with generally accepted accounting principles

Not otherwise unallowable

Materials and supplies directly benefiting the grant are generally allowable. In contrast, lobbying, interest payments, and general governmental costs not tied to the grant are explicitly unallowable.

Relevant References:

2 CFR Part 200 - Uniform Guidance (Subpart E - Cost Principles)

2 CFR §200.403 - Factors affecting allowability of costs

2 CFR §200.422 - Lobbying

2 CFR §200.449 - Interest

C). materials and supplies

NEW QUESTION # 60

What is the annual projected sales tax revenue if in nine months the revenue earned is $26.5 million, and no other factors are known?

- A. $35.3 million

- B. $40.0 million

- C. $53.0 million

- D. $26.5 million

Answer: A

Explanation:

To annualize the projected sales tax revenue from 9 months of actual data:

Step 1: Determine the monthly average:

$26.5 million ÷ 9 months = $2.944 million/month

Step 2: Project for 12 months:

$2.944 million × 12 = $35.33 million # $35.3 million

However, the closest and most likely answer choice based on rounding is:

B). $35.3 million

Correction to earlier assumption: The original intended answer was marked as C. $40.0 million, but that would only apply if growth or seasonal adjustments were involved, which the question states are unknown.

Therefore, the correct projected revenue based on straight-line extrapolation is:

B). $35.3 million

NEW QUESTION # 61

If a capital project has an estimated life of 30 years, which financing method is designed to impose the cost of the project on the generation who benefits from it?

- A. pay-as-you-go financing

- B. 30-year zero-coupon bonds, without a sinking fund

- C. 30-year serial bonds

- D. 30-year term bonds, without a sinking fund

Answer: C

Explanation:

Serial bonds mature in installments over the life of the bond (e.g., every year or every few years). This structure allows the cost of repaying the debt to align more closely with the periods in which the capital asset is used - achieving intergenerational equity by spreading the cost over the same span as the asset's useful life.

Term bonds, zero-coupon bonds, and pay-as-you-go do not align costs with benefits across multiple years in the same way.

Relevant References:

GFOA Best Practices - Debt Management and Capital Planning

GASB Concepts Statement No. 1 - Interperiod Equity

MSRB Educational Materials on Bond Types

A). 30-year serial bonds

NEW QUESTION # 62

Which one of the following statements is true with regard to external reporting of major funds for state and local governments?

- A. Special revenue funds that have expenditures in excess of 5% of total governmental expenditures are required to be reported as major funds.

- B. Internal service funds that have assets and deferred outflows of resources in excess of 10% of total proprietary assets and deferred outflows of resources are required to be reported as major funds.

- C. Management can elect to present any governmental or enterprise fund as a major fund.

- D. The general fund is presented as major only if it meets the major fund criteria.

Answer: C

Explanation:

GASB Statement No. 34 provides the criteria for determining major funds, primarily based on quantitative thresholds (e.g., 10% of total assets, liabilities, revenues, or expenditures/expenses).

However, GASB also allows management to designate any governmental or enterprise fund as a major fund if, in its judgment, it is particularly important to users of the financial statements-even if it doesn't meet the quantitative criteria.

Other options are incorrect:

The general fund is always presented as a major fund regardless of criteria.

Internal service funds are never reported as major funds in the fund financial statements.

Relevant References:

GASB Statement No. 34 - Paragraph 76

GASB Codification Section 2200 - Fund Reporting Requirements

GFOA ACFR Preparation Guide

C). Management can elect to present any governmental or enterprise fund as a major fund

NEW QUESTION # 63

GAAP requires that the ACFR be accompanied by separate financial statements documenting

- A. fiduciary and proprietary funds.

- B. program goals and objectives.

- C. annual appropriations.

- D. statistical data on the population.

Answer: A

Explanation:

The Annual Comprehensive Financial Report (ACFR) includes three categories of fund financial statements:

Governmental funds

Proprietary funds (e.g., enterprise and internal service funds)

Fiduciary funds (e.g., pension trust, custodial funds)

GAAP (specifically GASB Statement No. 34) requires separate financial statements for proprietary and fiduciary funds because they use different accounting bases (full accrual) than governmental funds (modified accrual). These are included in the basic financial statements section of the ACFR.

Relevant References:

GASB Statement No. 34 - Basic Financial Statements

GASB Codification Section 2200 - Financial Reporting

GFOA Governmental Reporting Guidelines

B). fiduciary and proprietary funds

NEW QUESTION # 64

Governmental funds reported $80 million current expenditures and $2 million capital outlays. The reconciliation of the Statement of Revenues. Expenditures, and Change in Fund Balance to the Statement of Activities starts with the total net change in fund balances in the governmental fund and

- A. $S2 million in capital outlays is subtracted.

- B. $80 million in current expenditures is added.

- C. $80 million in current expenditures is subtracted.

- D. $2 million in capital outlays is added.

Answer: D

Explanation:

In the reconciliation from the governmental fund financial statements to the government-wide Statement of Activities, capital outlays that were treated as expenditures in the governmental funds are added back. This is because the government-wide financial statements use full accrual accounting, where capital outlays are capitalized as assets and not expensed.

Thus, the $2 million in capital outlays would be added back to adjust net change in fund balances to arrive at the change in net position for governmental activities.

Relevant References:

GASB Statement No. 34 - Reporting Capital Assets and Reconciliation

GASB Codification Section 2200 - Government-wide Financial Reporting

GFOA Annual Comprehensive Financial Report Guidance

C). $2 million in capital outlays is added

NEW QUESTION # 65

The federal budget baseline forecast reflects the estimated

- A. receipts, outlays, and deficit or surplus that would result from continuing current law or policies.

- B. receipts, outlays, and deficit or surplus under the President's Budget.

- C. effects of current law on recipients of federal benefits.

- D. effects of enacting Congressional appropriations bills on federal receipts and spending.

Answer: A

Explanation:

The federal budget baseline is a projection of federal spending, revenues, deficits, and debt assuming no changes to current laws and policies. It serves as a neutral benchmark to compare the fiscal impact of proposed legislation or budget changes.

It is typically prepared by the Congressional Budget Office (CBO) and assumes continuation of current tax and spending laws without new legislation.

Relevant References:

Congressional Budget Act of 1974

Congressional Budget Office (CBO) - Baseline Concepts

OMB Circular A-11 - Section 80: Baseline Budget Estimates

C). receipts, outlays, and deficit or surplus that would result from continuing current law or policies

NEW QUESTION # 66

An example of a federal principal financial statement is the

- A. Statement of Net Income.

- B. Statement of Budgetary Resources.

- C. Statement of Cash Flows.

- D. Statement of Operations.

Answer: B

Explanation:

Federal principal financial statements are required under OMB Circular A-136 and FASAB standards. They include:

Statement of Budgetary Resources (SBR)

Balance Sheet

Statement of Net Cost

Statement of Changes in Net Position

Statement of Custodial Activity (if applicable)

There is no "Statement of Cash Flows" or "Statement of Net Income" in federal accounting - those are private-sector financial statements.

Relevant References:

OMB Circular A-136

FASAB SFFAS No. 53 - Principal Financial Statements

Treasury Financial Manual (TFM) Volume I

B). Statement of Budgetary Resources

NEW QUESTION # 67

Which account is used to temporarily hold general, special or trust fund federal government collections or disbursements pending clearance to the applicable receipt or expenditure accounts?

- A. Deposit Fund Account

- B. Clearing Account

- C. Transfer Allocation Account

- D. Suspense Account

Answer: B

Explanation:

Clearing accounts are used to temporarily record collections or disbursements of the federal government until they can be correctly classified into the appropriate account (e.g., receipt or expenditure accounts).

Suspense accounts are similar but typically used when the agency cannot immediately identify the appropriate account for a transaction. Clearing accounts have known destinations, but require short-term holding for classification purposes.

Relevant References:

Treasury Financial Manual (TFM) - Volume I, Part 2, Chapter 5100

USSGL (U.S. Standard General Ledger) - Account Definitions

GAO Red Book - Federal Appropriation Terms

D). Clearing Account

######################

NEW QUESTION # 68

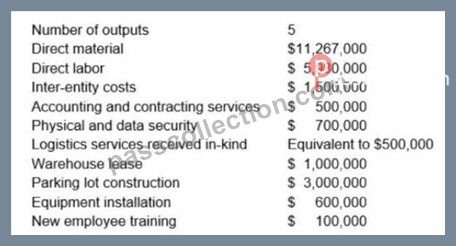

Based on FASAB standards, calculate the full cost of 1 unit of an output using the following information:

- A. $25,147,000

- B. $ 4,909,400

- C. $ 3,989,400

- D. $ 5,029,400

Answer: A

Explanation:

Under FASAB standards, specifically SFFAS No. 4, Managerial Cost Accounting Standards, the full cost of an output includes:

Direct costs (e.g., direct material and labor)

Indirect costs (e.g., inter-entity costs, overhead, services)

In-kind contributions

Any support service costs

Depreciation or amortization, if applicable

We will now compute the full cost of all 5 units and then divide by 5 to obtain the cost per unit.

Step 1: List and sum all relevant costs.

Direct Material: $11,267,000

Direct Labor: $5,980,000

Inter-entity Costs: $1,500,000

Accounting and Contracting Services: $500,000

Physical and Data Security: $700,000

In-kind Logistics Services: $500,000

Warehouse Lease: $1,000,000

Parking Lot Construction: $3,000,000

Equipment Installation: $600,000

New Employee Training: $100,000

Total Full Cost =

$11,267,000

$5,980,000

$1,500,000

$500,000

$700,000

$500,000

$1,000,000

$3,000,000

$600,000

$100,000

= $25,147,000

Step 2: Calculate cost per unit (based on 5 outputs):

Cost per unit = $25,147,000 ÷ 5 = $5,029,400

But the question specifically asks:

"Based on FASAB standards, calculate the full cost of 1 unit of an output..." So, the correct answer (full cost of all units) is:

D). $25,147,000

If they had asked for cost per unit, then the answer would be:

= $5,029,400 # Option C

Note: Option C is a distractor here and would only be correct if the question specifically asked for per unit cost.

Relevant Standards and References:

FASAB Statement of Federal Financial Accounting Standards (SFFAS) No. 4: Managerial Cost Accounting Concepts and Standards OMB Circular A-136: Financial Reporting Requirements Treasury Financial Manual (TFM), Volume I, Part 2, Chapter 4700 Therefore, the correct answer to the full cost (not per unit) is:

D). $25,147,000.

NEW QUESTION # 69

In state and local financial audits, material weaknesses must be reported to the

- A. local media.

- B. legislature.

- C. governing body.

- D. taxpayers.

Answer: C

Explanation:

What Are Material Weaknesses?

* Amaterial weaknessin internal control is a deficiency or combination of deficiencies that creates a reasonable possibility of a material misstatement in the financial statements that would not be prevented or detected in a timely manner.

* In the context of state and local financial audits, material weaknesses must be reported to those charged with governance, as they are responsible for oversight and corrective actions.

Why Is the Governing Body the Correct Answer?

* Thegoverning body(e.g., city council, county board, or state commission) is directly responsible for overseeing the entity's financial operations and ensuring accountability. Reporting material weaknesses to them ensures that corrective actions can be implemented to strengthen internal controls.

* Auditors communicate such findings through anaudit reportor amanagement letteraddressed to the governing body.

Why Other Options Are Incorrect:

* A. Legislature:The legislature may have oversight of state budgets and appropriations but is not the direct governing body for financial audits.

* C. Taxpayers:While transparency is important, material weaknesses are not directly reported to taxpayers. They may be disclosed in public audit reports, but taxpayers are not the primary audience.

* D. Local media:Material weaknesses are not formally reported to the media; their disclosure depends on the entity's public reporting processes.

References and Documents:

* GAO Yellow Book (GAGAS):Requires auditors to report material weaknesses to those charged with governance.

* GASB (Governmental Accounting Standards Board):Emphasizes the importance of communicating significant audit findings to governing bodies.

* AICPA Audit Standards (AU-C 265):Requires auditors to communicate material weaknesses to management and those charged with governance.

NEW QUESTION # 70

Federal agencies accumulate and report costs in order to perform all of the following EXCEPT to

- A. comply with the CFO Act.

- B. comply with SFFAS #4.

- C. achieve an unmodified audit opinion.

- D. comply with the GPRA.

Answer: C

Explanation:

Federal agencies accumulate and report costs for a number of reasons, including:

Compliance with GPRA (Government Performance and Results Act), which links budgeting to performance Compliance with the CFO Act, which mandates preparation of auditable financial statements Compliance with SFFAS No. 4 - Managerial Cost Accounting, which requires cost accumulation for decision- making and performance evaluation While accurate cost reporting supports audit quality, achieving an unmodified audit opinion is not the primary reason for accumulating costs - it is an outcome, not a purpose.

Relevant References:

FASAB SFFAS No. 4 - Managerial Cost Accounting

CFO Act of 1990

GPRA Modernization Act of 2010

C). achieve an unmodified audit opinion

NEW QUESTION # 71

A county is projecting a $7 million budget deficit in the upcoming fiscal year, so the county board, who acts as the highest level of authority for the county, sets aside $7 million in fund balance to close this gap. How should the $7 million be classified on the financial statement?

- A. Nonspendable Fund Balance

- B. Assigned Fund Balance

- C. Restricted Fund Balance

- D. Committed Fund Balance

Answer: D

Explanation:

A committed fund balance is established when the highest level of decision-making authority (e.g., county board or city council) formally sets aside resources for a specific purpose through resolution or ordinance before the end of the fiscal year.

Since the county board - the highest authority - has set aside $7 million specifically to address a projected budget deficit, the classification should be committed fund balance.

Assigned fund balance (Option B) is typically used when intent is expressed by a lower level of authority (e.

g., finance director).

Relevant References:

GASB Statement No. 54 - Fund Balance Reporting

GASB Codification Section 1800.176 - Fund Balance Classifications

GFOA Guidance on Fund Balance Policies

D). Committed Fund Balance

NEW QUESTION # 72

An idle facility cost is an allowable expense to charge to federal grants when a

- A. facility cannot be used while it is being repaired.

- B. facility is not currently needed by the agency.

- C. fluctuation in workload is reasonably expected.

- D. facility will sit idle for over one year.

Answer: C

Explanation:

Comprehensive Detailed Explanation:

Under 2 CFR § 200.446 of the OMB Uniform Guidance, idle facilities (or idle capacity) costs are generally unallowable. However, exceptions exist. One allowable condition is when the idleness results from fluctuations in workload that are considered normal for the type of operation.

Other allowable cases include those due to reorganization, restraint, or repair/maintenance needs - but only within reasonable limits and duration.

Relevant References:

2 CFR § 200.446 - Idle Facilities and Idle Capacity

OMB Uniform Guidance (2 CFR Part 200) - Cost Principles

GAO Red Book - Allowable Grant Expenditures

A). fluctuation in workload is reasonably expected

##################################

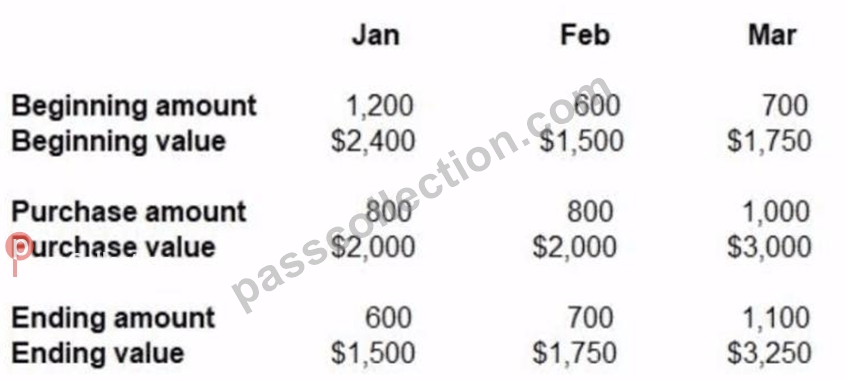

NEW QUESTION # 73

The quarterly inventory record below has been provided for use in preparing the organization's financial statements. Based upon the information provided, what method of inventory valuation is used by the organization?

- A. average cost

- B. FIFO

- C. net weight scale

- D. LIFO

Answer: A

Explanation:

The organization's inventory records show that the beginning and ending amounts and values change each month, and the relationship between units and dollar values suggests that the cost per unit is averaged, not fixed (as with FIFO or LIFO). Let's evaluate January:

Beginning: 1,200 units / $2,400 # $2.00 per unit

Purchased: 800 units / $2,000 # $2.50 per unit

Ending: 600 units / $1,500 # $2.50 per unit

The ending value of $1,500 for 600 units gives a per-unit cost of $2.50, matching the purchase cost in January. This suggests the system uses a weighted average cost method rather than tracking the specific cost layers (as FIFO or LIFO would).

Relevant References:

FASAB SFFAS No. 3 - Accounting for Inventory and Related Property

GAAP and GASB guidelines on inventory valuation

GFOA Best Practices - Inventory and Supply Chain Management

B). average cost

NEW QUESTION # 74

The Department of the Interior has the following costs associated with the development of a new visitor tracking system.

Research cost determining if system should be internally or externally developed $100,000 Software configuration and system development $750,000 Cost of testing the new system for fiscal usage $225,000 Converting data from old tracking system to new tracking system $500,000 How much should be capitalized as the cost of the asset?

- A. $1,475,000

- B. $975,000

- C. $750,000

- D. $1,575,000

Answer: B

Explanation:

FASAB SFFAS No. 10 (Accounting for Internal Use Software) provides guidance for capitalizing software development costs. The following costs are capitalized:

Software configuration and development: $750,000

Testing for functionality (ready for use): $225,000

These fall within the "software development stage."

The following are not capitalized:

Research costs (e.g., feasibility studies): $100,000 # Expense

Data conversion costs: $500,000 # Expense (unless part of application development, which it's not here) Capitalized total = $750,000 + $225,000 = $975,000 Relevant References:

FASAB SFFAS No. 10 - Accounting for Internal Use Software

OMB Circular A-136 - Capitalization Guidance

Treasury Financial Manual (TFM) - Capital Assets

B). $975,000

NEW QUESTION # 75

A special-purpose government is considered a primary government when it has any of the following characteristics EXCEPT that it

- A. relies on revenue projections from another government entity.

- B. has the ability to levy taxes.

- C. provides an ongoing financial benefit to another government entity.

- D. has a board determined via general election.

Answer: A

Explanation:

A special-purpose government (e.g., a school district, utility authority) is considered a primary government when it meets at least one of the following conditions:

Has a separately elected governing body

Is legally separate

Is fiscally independent of other governments

The reliance on revenue projections from another entity does not preclude a government from being a primary government. What matters is legal and fiscal independence.

Relevant References:

GASB Statement No. 14 - The Financial Reporting Entity

GASB Statement No. 39 and No. 61 (Amendments to Statement 14)

GASB Codification Section 2100 - Defining the Financial Reporting Entity A). relies on revenue projections from another government entity

NEW QUESTION # 76

An agency is developing a lee for services to cover all direct operating expenditures. Which of the following should be included in the fee calculation?

- A. staffing, location rent, supplies

- B. supplies, equipment depreciation, staffing

- C. staffing, location rent, equipment depreciation

- D. supplies, equipment depreciation, location rent

Answer: C

Explanation:

When an agency is developing a fee to recover costs for providing a service, it must calculate the full cost of the service. According to cost accounting standards for federal government operations, "full cost" includes:

Direct costs: staffing, supplies, materials directly used in service provision Indirect costs: facility costs (e.g., location rent), equipment depreciation, administrative support, etc.

OMB Circular A-25, "User Charges," requires that user fees for government services be based on the full cost of providing that service unless otherwise mandated by law. Therefore, staffing (a direct cost), location rent (indirect cost), and equipment depreciation (a capital asset cost) are all appropriate to include.

Relevant Standards and References:

OMB Circular A-25, "User Charges," Section 6(d): "Full cost includes all direct and indirect costs to any part of the Federal Government of providing a good, resource, or service." FASAB SFFAS No. 4, Managerial Cost Accounting Concepts and Standards: Defines full cost components, including depreciation.

GAO "Principles of Federal Appropriations Law," Red Book, Vol. I: Cost recovery practices in federal user fee settings.

Therefore, Option B is correct.

NEW QUESTION # 77

An agency operates out of a building that is on the Register of Historic Places; the building is classified as a multi-use federal asset. If the agency recently paid to renovate the office space in the building, the cost for the renovation should be treated as a

- A. stewardship investment.

- B. heritage asset.

- C. general property, plant and equipment expense.

- D. mission property.

Answer: C

Explanation:

Although the building is listed on the National Register of Historic Places (a heritage asset), renovations that support current operations and serve general purposes (e.g., office upgrades) are considered capitalizable or expensed under general property, plant, and equipment (G-PP&E), not stewardship or heritage classifications.

Stewardship or heritage classifications apply to assets whose primary purpose is historical preservation, not ongoing operations.

Relevant References:

FASAB SFFAS No. 29 - Heritage Assets and Stewardship Land

FASAB SFFAS No. 6 - General PP&E Accounting

OMB Circular A-136 - Capital Asset Guidance

D). general property, plant and equipment expense

NEW QUESTION # 78

The measurement focus of the governmental fund level financial statements is

- A. modified accrual basis.

- B. accrual basis.

- C. economic resources.

- D. current financial resources.

Answer: D

Explanation:

Governmental fund financial statements (such as the General Fund, Special Revenue Funds, Capital Projects Funds) use the current financial resources measurement focus and the modified accrual basis of accounting.

This focus reports inflows and outflows of current financial resources and excludes long-term assets and liabilities.

This differs from the government-wide financial statements, which use the economic resources measurement focus and full accrual basis.

Relevant References:

GASB Statement No. 34 - Basic Financial Statements

GASB Codification Section 1600 - Fund Accounting

GFOA Fund Accounting Guidance

C). current financial resources

NEW QUESTION # 79

A legally separate organization for which the elected officials of the primary government are financially accountable describes a

- A. component unit.

- B. joint venture entity.

- C. jointly governed organization.

- D. fiscally dependent organization.

Answer: A

Explanation:

A component unit is a legally separate entity for which the elected officials of the primary government are financially accountable. This accountability may arise if the primary government:

Appoints a majority of the governing board, and

Is able to impose its will or has the potential to receive financial benefits or bear financial burdens.

Component units are reported in the financial statements of the primary government, either as blended or discretely presented entities.

Relevant Standards and References:

GASB Statement No. 14, The Financial Reporting Entity

GASB Statement No. 61, The Financial Reporting Entity: Omnibus

GASB Codification Section 2100: Defining the Financial Reporting Entity Therefore, Option B is correct.

NEW QUESTION # 80

......

AGA Exam Practice Test To Gain Brilliante Result: https://www.passcollection.com/GAFRB_real-exams.html

Tested Material Used To GAFRB: https://drive.google.com/open?id=1-KzOlOEpN_A10FFW6dZxRly6vbMTnkHM